The Hong Kong University of Science and Technology Value Partners Center for Investing has examined the performance of value stocks in the Japanese stock market over the period January 1975 to December 2011. They have also broken out the performance of value stocks during Japan’s long-term bear market over the 1990 to 2011 period, when the stock market dropped 62.21 percent.

The white paper Performance of Value Investing Strategies in Japan’s Stock Market examines the performance of equal-weight and market capitalization weighted quintile portfolios of five price ratios–price-to-book value, dividend yield, earning-to-price, cash flow-to-price, and leverage-to-price—excluding the smallest 33 percent of stocks by market capitalization.

The portfolios were rebalanced monthly over the full 37 years.

The authors find the value quintile of equal-weighted portfolios book-to-market, dividend yield, earning-to-price, cash flow-to-price, and leverage-to-price generated monthly returns of 1.48 percent (19.3 percent per year), 1.34 percent (17.3 percent per year), 1.78 percent (23.6 percent per year), 1.66 percent (21.8 percent per year) and 0.78 (9.8 percent per year) percent in the 1975–2011 period.

The returns diminished over the 1990 to 2011 period. The value quintile of equal-weighted portfolios book-to-market, dividend yield, earning-to-price, cash flow-to-price, and leverage-to-price generated monthly returns of 0.84 percent (10.6 percent per year), 0.78 percent (9.8 percent per year), 1.31 percent (16.9 percent per year), 1.13 percent (14.4 percent per year) and 0.0 percent (0.0 percent per year) in the 1990–2011 period, respectively. In contrast, the Japanese stock market lost 62.21 percent.

They find similar results for market capitalization-weighted portfolios sorted by these measures, as well as for three-, six-, nine-, and twelve-month holding periods (excluding the leverage-to-price ratio).

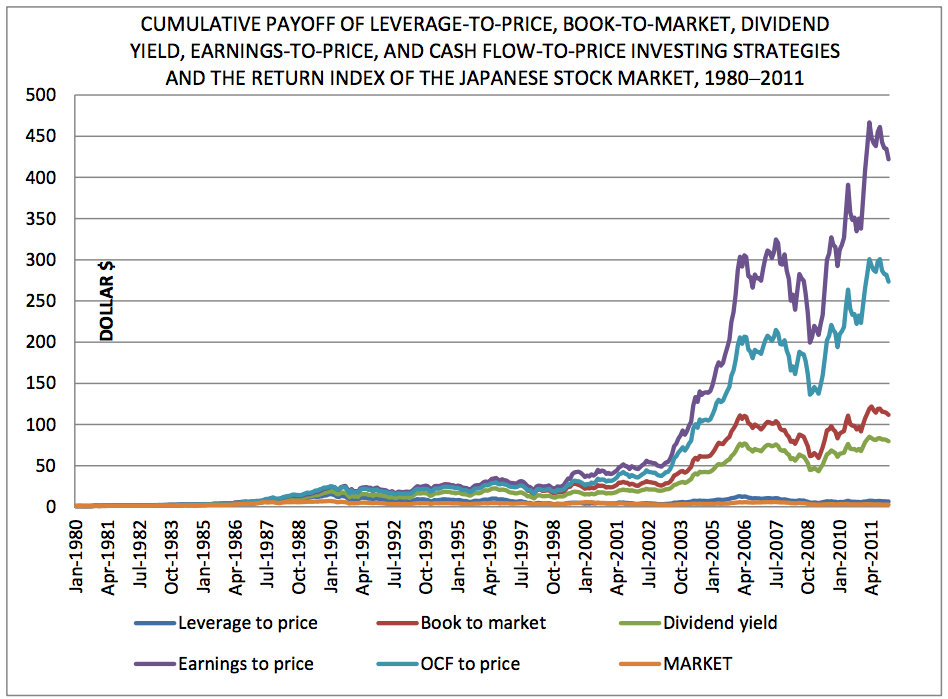

They also investigated the cumulative payoff in dollar terms of investing $1 in the portfolios having the highest values of our value measures with monthly portfolio rebalancing in the 1980–2011 period. Value investing strategies based on stock’s book-to-market, dividend yield, earning-to-price , cash flow-to-price , and leverage-to-price grew $1 into $115.98, $81.88, $433.86, $281.49, and $6.62 respectively, while the aggregate stock market turned $1 into a mere $2.76, in the 1980–2011 period. This implies that these value investing strategies rewarded investors 42.0, 29.6, 157, 102 and 2.40 times what the Japanese stock market did. The effective monthly compound returns of the various investing strategies are 1.25 percent, 1.16 percent, 1.60 percent, 1.48 percent and 0.49 percent, while the aggregate stock market only delivered 0.27 percent in this period.

Four out of five value investing strategies actually rewarded investors with positive returns in the bear market that spanned two decades from 1990 to 2011, turning $1 into $4.77, $4.25, $17.17, and $10.91, implying profits of 377 percent, 325 percent, 1617 percent, and 991 percent respectively, while the stock market plunged 62.21 percent after reaching its peak in January 1990. In addition, every one of these value investing strategies continued to generate positive returns between the pre-global financial crisis peak in 2007 and December 2011.

Order Quantitative Value from Wiley Finance, Amazon, or Barnes and Noble.

Click here if you’d like to read more on Quantitative Value, or connect with me on LinkedIn.