Great piece from Tocqueville Funds’ François Sicart called Contrarian Investing in a Liquidity-Driven Environment. Tocqueville is a “bottom-up” value investor:

Individual stock selection prevails over macro opinions, be they about the economy or the markets.

This approach generally has been vindicated in the past, as value investors tended to outperform a majority of money managers over full market cycles; and this outperformance has been achieved principally during bear markets, by losing less than most. The reason, I believe, is so obvious as to sound simplistic: When a stock is selling close to the “intrinsic” value of its underlying company’s shares, it does not have to travel down very much to find a floor.

Good logic, but it didn’t protect Tocqueville of anyone else in 2007 to 2009:

In spite of this “unquestionable” logic, the great majority of portfolios (including those of some iconic value investors) were engulfed in the panicky downward spiral that followed the Lehman Bros. failure, between the summer of 2008 and the final bottom, in early 2009.

…

That part of the overall 53-percent decline from the 2007 top to the 2009 bottom was generally indiscriminate – more so than I can remember throughout my career, with the possible exception of the one-day crash of 1987; but that violent but brief market episode did not trigger a global financial crisis or recession.

“But it’s a market of stocks”:

At this stage of a discussion, a broker would typically tell you, “This is not a stock market, but a market of stocks,” implying that there are always attractive investments somewhere, even when the overall market seems overpriced. And although this is a typical sales pitch, they usually are correct. This time, however, we may have to work harder to find those attractive investments.

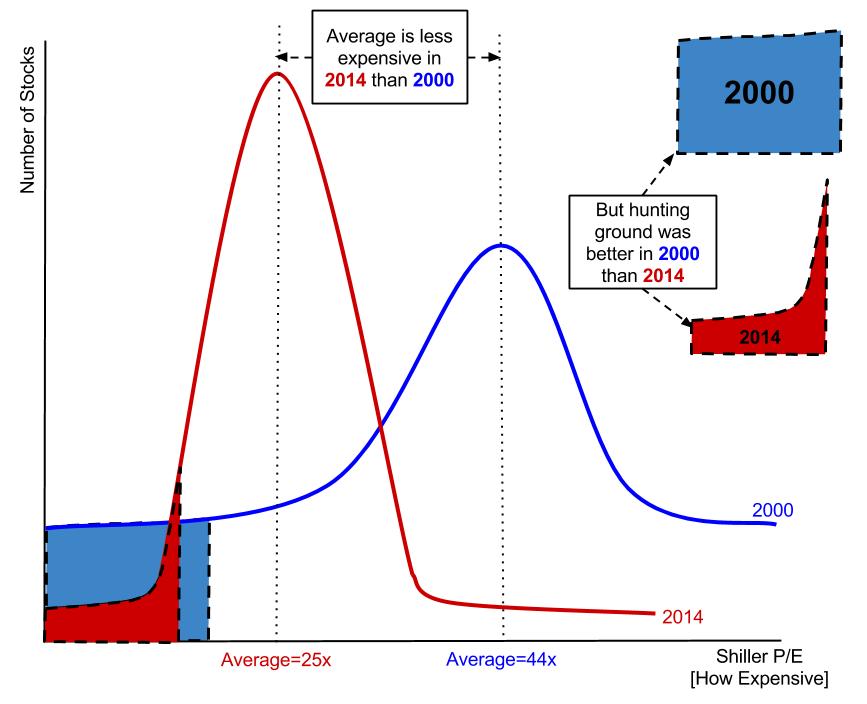

David Kostin, Goldman Sachs’ chief U.S. equity strategist, explained that investor demand for “value” has been so pervasive that low-valuation stocks had outperformed higher valuation peers by 12 percent in 2013. As a result, the distribution of S&P 500 P/E multiples was now its tightest in at least 25 years, implying less differentiation of companies based on valuation.

“With valuation clustered together, we believe there are attractive relative value opportunities where companies with different fundamentals are trading at very similar valuation levels.”

If you’re having trouble finding undervalued stocks, this is some indication that it’s not just you. The current valuation spread is narrower than it was in 2007, and stands in stark contrast to the early 2000s when it was wider than usual.

Read Tocqueville Funds’ Contrarian Investing in a Liquidity-Driven Environment.

h/t Farnam Street Investments.

Order Quantitative Value from Wiley Finance, Amazon, or Barnes and Noble.

Click here if you’d like to read more on Quantitative Value, or connect with me on LinkedIn.

Read Full Post »