Source: “What Goes Up Must Come Down!” James Montier (March 2012)

In his recent piece The Endgame is Forced Liquidation John Hussman eloquently describes the reason why investors need to be wary of structural arguments intended to dispose of indicators with a very reliable cyclical record:

On the temptation to disregard proven indicators

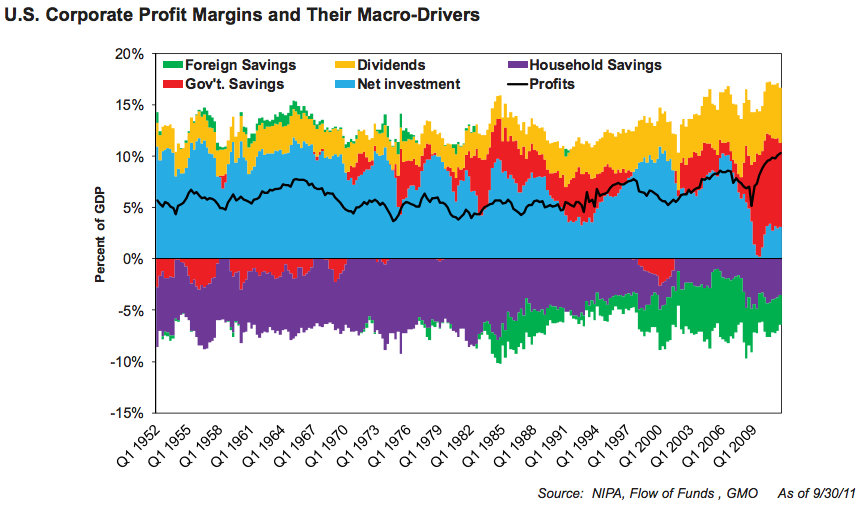

As a side-note, it’s important for investors to be wary of “structural” arguments intended to discard indicators that have very reliable cyclical records. For example, hardly a day goes by that we don’t see an attempt to harness some long-term structural factor, such as increasing globalization of trade, to explain away the spike in profit margins over the past few years – in the hope of proving that these margins will be permanent this time. Some of these arguments are discussed in recent weekly comments. But these factors don’t explain the cyclical fluctuations in profit margins at all, and can’t be used to discard the accounting relationships and decades of evidence that corporate profits have a strong secular and tight cyclical mirror-image relationship with the combined total of government and household savings.

Investors get themselves in trouble when they embrace “new economy” theories not because those new theories can be demonstrated in the data; not because existing approaches fail to fully explain the subsequent historical outcomes; but solely because time-tested approaches suggest uncomfortable outcomes in the present instance.

The same sort of structural second-guessing is evident in the gold market here – a good example of what forced liquidation looks like, as my impression is that leveraged longs have been forced into a fire-sale in recent weeks, creating good values for longer-term investors, but with continued near-term risks. If we look at the ratio of gold prices to the Philadelphia gold index (XAU), we do believe there are structural factors that affect that ratio (primarily the increasing cost of extracting gold over time). But these don’t explain away or eliminate the strong cyclical relationship between the gold/XAU ratio and subsequent returns on the XAU over the following 3-4 year periods. So while we don’t believe that the record high gold/XAU ratio can be taken entirely at face value, there’s no question that it is elevated even on a cyclical basis (that is, even allowing for a gradual structural increase over time), and there’s no question in the data that cyclically elevated gold/XAU ratios have been associated with strong subsequent gains in the XAU index over a 3-4 year period on average, though certainly not without risk or volatility.

As a final example, some analysts (such as the Dow 36,000 authors) have argued that the proper risk premium on stocks, relative to Treasury securities, should be zero. This line of argument was used in 2000 to suggest that stocks were still cheap despite high apparent valuations. But this “secular” argument for high valuations ultimately did not weaken the long-term evidence and tight cyclical relationship between valuations and subsequent market returns. Despite all the new economy arguments about productivity growth, the internet, globalization, the great moderation, and the outdated relevance of risk premiums, stocks still went on to lose half their value over the next two years, and to produce negative returns over the decade that followed.

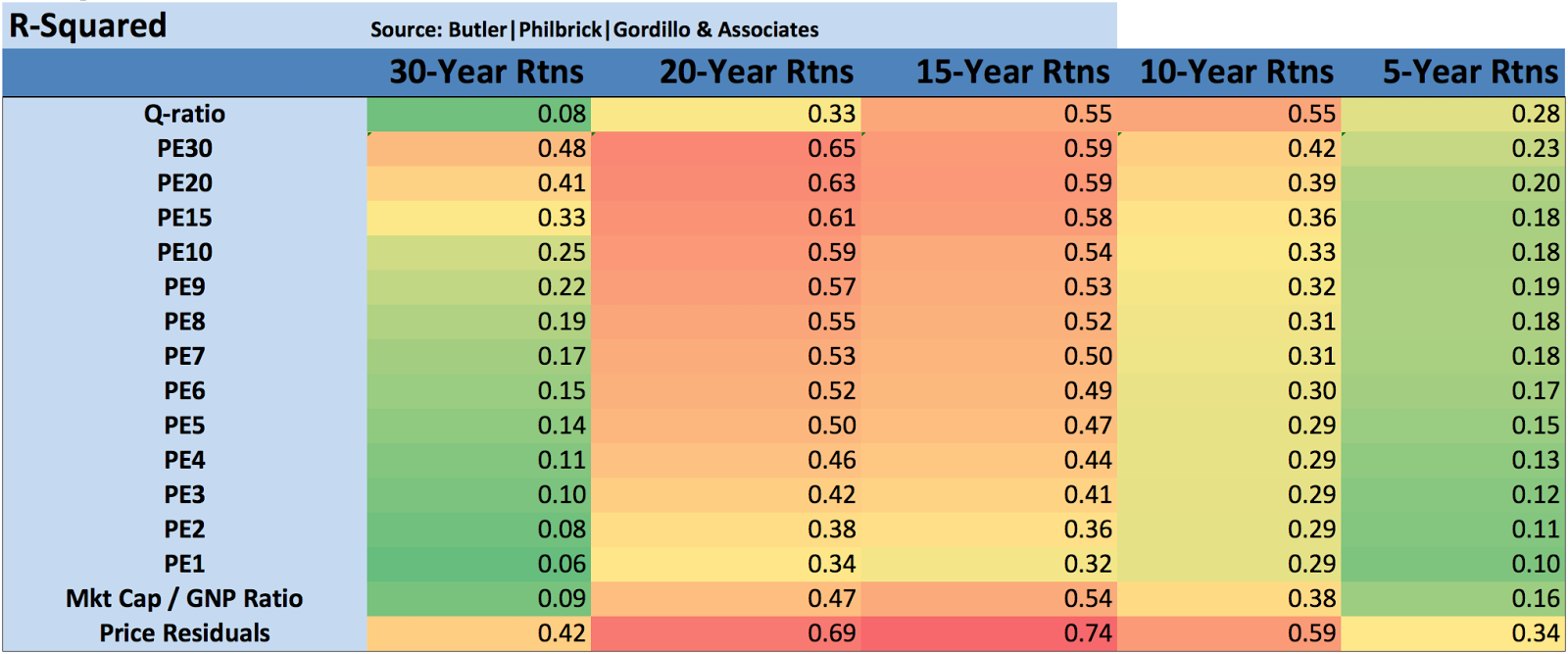

The bottom line is that it becomes very tempting – both in speculative markets and fearful ones – to discard well-proven indicators as meaningless by arguing that some “structural” change in the market or the economy makes things different this time. True, those arguments can sometimes be used to explain very long-term changes in the level of an indicator. But even then, new economy arguments are typically ineffective at explaining away the informative cyclical variations in good indicators. Be particularly hesitant about ignoring indicators whose cyclical variations have been effective even in recent data, as is true of the ability of time-tested valuation approaches to explain subsequent 10-year market returns even during the period since the late-1990’s, and the ability of government and household savings to tightly explain cyclical swings in profit margins and subsequent profit growth, even in the most recent economic cycle.

Order Quantitative Value from Wiley Finance, Amazon, or Barnes and Noble.

Click here if you’d like to read more on Quantitative Value, or connect with me on LinkedIn.

h/t Joe