David Ogilvy as he appears in Ogilvy on Advertising

In my first year of law school I worked as a junior copywriter in an advertising agency. The two founders of the agency were famous for a series of iconic beer commercials that ran in the 1980s featuring sports stars, bikini-clad women, sun, surf and sand. All standard fare for beer ads in the ’80s. What made these advertisements iconic was the jingle, the writing and singing of which was the specialty of the founders. Legend had it that they produced the jingles under the influence of the product, which of course only helped their myth grow.

This had all passed into folklore by the time I got there. In the late 1990s it was a mostly corporate environment. Mostly. There were still a few refugees from the ’80s, and a few young guys who wished that the ’80s lived on. Grinding out copy 9-to-5, Monday-to-Friday is a great way to become a solid writer while getting paid. All the guys I sat with were smart, and funny and very good writers. What makes a good writer? As Bo says in Get Shorty:

There’s nothin’ to know. You have an idea, you write down what you wanna say. Then you get somebody to add in the commas and shit where they belong, if you aren’t positive yourself. Maybe fix up the spelling where you have some tricky words . . . although I’ve seen scripts where I know words weren’t spelled right and there was hardly any commas in it at all. So I don’t think it’s too important. Anyway, you come to the last page you write in ‘Fade out’ and that’s the end, you’re done.

In response, John Travolta’s Chili Palmer deadpans, “That’s all there is to it? Then what do I need you for?”

It’s deceptively simple, but good writing is really hard. I didn’t know much when I got to the agency, but I knew that I didn’t know how to write copy. I asked around for a good book to read. Someone told me Ogilvy on Advertising was the bible. (It still is. Everyone should read it. It’s the copywriter’s Intelligent Investor.) I bought it and read it. And it intimidated me. Ogilvy is an extraordinarily good writer. You’d expect nothing less from a man who made his living writing words that persuaded other people to pay him lots of money to write words for them.

I still have my original copy of Ogilvy on Advertising, ripped and soaked through with coffee. It begins in the Overture:

I do not regard advertising as entertainment or an art form, but as a medium of information. When I write an advertisement, I don’t want you to tell me that you find it ‘creative’. I want you to find it so interesting that you buy the product. When Aeschines spoke, they said, ‘How well he speaks’. But when Demosthenes spoke, they said, ‘Let us march against Philip.’

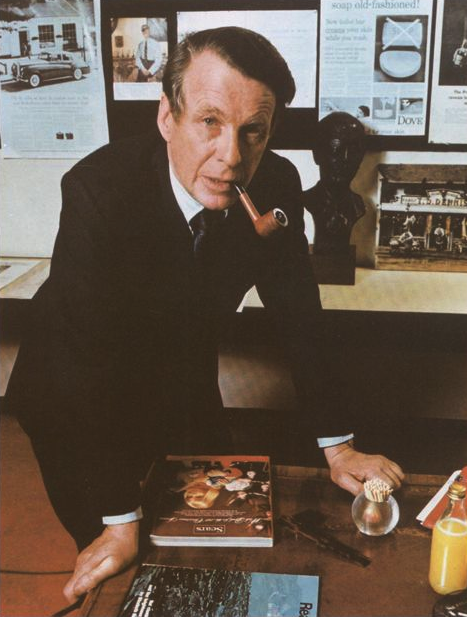

The call out on the first page reads, “I run the risk of being denounced by the idiots who hold that any advertising technique which has been in use for more than two years is ipso facto obsolete.” The photo above appears on the facing page: Ogilvy in suit-and-tie leaning over his desk, pipe clenched between his teeth, all aggressive mien under perfectly coiffed hair. It was heady stuff for a kid. I lapped it up. In my mind, Ogilvy was a Hemingway-esque character, writing, drinking and fighting his way around the world. (That’s no great stretch. His autobiography is called Blood, Brains and Beer.) I wanted to be Ogilvy. If I’m honest, I still want to age into Ogilvy.

What does this have to do with investing?

Ogilvy was a pioneer in the use of research about advertising and behavioral psychology to make ads that persuade people to buy.

Back to the Overture. Ogilvy writes:

I am sometimes attacked for imposing ‘rules’. Nothing could be further from the truth. I hate rules. All I do is report on how consumers react to different stimuli. I may say to a copywriter, ‘Research shows that commercials with celebrities are below average in persuading people to buy products. Are you sure you want to use a celebrity?’ Call that a rule? Or I may say to an art director, ‘Research suggests that if you set the copy in black type on a white background, more people will read it than if you set it in white type on a black background.’ A hint, perhaps, but scarcely a rule.

Though I eventually abandoned advertising for law school exams, I’ve never abandoned Ogilvy. I believe that that research about investing and simple rules to combat behavioral errors are essential to good fundamental investment.

Research lets you know, for example, that using forward earnings estimates is a bad idea. Research also shows that screening for good five-year earnings growth leads to below average returns. And it also hints that return on equity is a misleading metric.

And simple rules combat behavioral errors. David Ogilvy passed away in 1999, but the Ogilvy Group, the firm he founded, adheres to his philosophy. Rory Sutherland, the vice-chairman of Ogilvy Group UK is a self-described “champion of the application of behavioral economics in advertising.” Sutherland believes that we are more likely to follow simple, absolute rules—“if X, then Y”—that work with our nature than others that are subtle, and require a “continuous exercise of self-restraint:”

Let’s consider the old rule of restricting yourself to a maximum number of units of alcohol a week. It demands constant vigilance. It often requires you to stop drinking while drunk. And it is fiendishly easy to cheat: you simply convince yourself that a 25cl glass of 14.7 per cent Chilean Merlot is one unit when it is really three. Better men than us have deceived themselves this way: Immanuel Kant rationed himself to one pipe of tobacco after breakfast; he stuck to his rule, but friends noticed that by the end of his life, all his pipes were enormous.

Sutherland’s observation applies equally to investing. Value investors follow a simple algorithm that states something like the following: Buy if market price is equal to or less than some fixed discount from intrinsic value. Sell if market price is equal to or exceeds intrinsic value. Graham’s net current asset value rule for acquiring sub-liquidation stocks is an example of such a simple, unambiguous investment strategy; simple to calculate, with concrete rules for its application. Graham recommended it as a “foolproof method of systematic investment—once again, not on the basis of individual results but in terms of the expectable group outcome.”

The net current asset value calculation couldn’t be simpler: Net current asset value equals current assets less all liabilities. And the rules couldn’t be more concrete: Buy if market price is two-thirds of net current asset value or less. Sell if market price has risen 50 percent, or two years have elapsed since acquisition, whichever occurs first. The returns to the net current asset value rule are astronomical. The problem with it is that it is very limited in its application. Few stocks pass its “buy” criteria in an ordinary market. It is possible, however, to apply the underlying philosophy without employing the actual rule. We can calculate intrinsic value in any number of ways, and apply the same directive.

This is all that is meant by a rule. At root, it is simply an exhortation to adhere strictly to the philosophy of value investment: Buy only if market price is some fixed discount from intrinsic value or less, pass otherwise. Sell only if market price is equal to or greater than intrinsic value, or a better opportunity can be found, hold otherwise.

I discuss these ideas–the use of research to identify counterintuitive, but predictive value investment principles, and the application of simple, unambiguous rules to combat behavioral errors–and many more in my new book Deep Value: Why Activist Investors and Other Contrarians Battle for Control ofLosing Corporations (hardcover, 240 pages, Wiley Finance).

Buy the book from Wiley Finance, Amazon, or Barnes and Noble.

Click here if you’d like to read more on Deep Value, or connect with me on Twitter, LinkedIn or Facebook.