Robert Novy-Marx, whose The Other Side of Value paper we quoted from extensively in Quantitative Value, has produced another ripping paper called The Quality Dimension of Value Investing (.pdf). Novy-Marx argues that value investment strategies that seek high quality stocks are “nearly as profitable as traditional value strategies based on price signals alone.”

Accounting for both dimensions by trading on combined quality and price signals yields dramatic performance improvements over traditional value strategies. Accounting for quality also yields significant performance improvements for investors trading momentum as well as value.

Novy-Marx’s The Other Side of Value paper showed that a simple quality metric, gross profits-to-assets, has roughly as much power predicting the relative performance of different stocks as tried-and-true value measures like book-to-price.

Buying profitable firms and selling unprofitable firms, where profitability is measured by the difference between a firm’s total revenues and the costs of the goods or services it sells, yields a significant gross profitability premium.

Most intriguingly, Novy-Marx finds that “the signal in gross profits-to-assets is negatively correlated with that in valuation ratios.”

High quality firms tend to trade at premium prices, so value strategies that trade on quality signals (i.e., quality strategies) hold very different stocks than value strategies that trade on price signals. Quality strategies tilt towards what would traditionally be considered growth stocks. This makes quality strategies particularly attractive to traditional value investors, because quality strategies, in addition to delivering significant returns, provide a hedge to value exposures.

Novy-Marx argues that investors can “directly combine the quality and value signals and, in line with Graham’s basic vision, only buy high quality stocks at bargain prices. By trading on a single joint profitability and value signal, an investor can effectively capture the entirety of both premiums.”

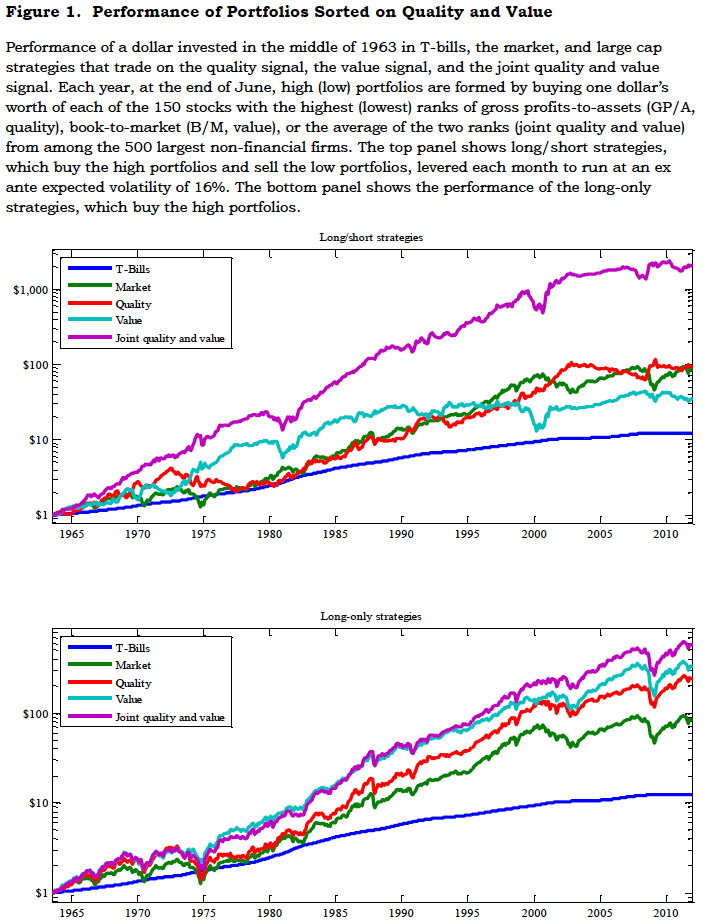

Performance of Quality, Value and Joint Strategies

(Click to enlarge).

Figure 1 shows the performance of a dollar invested in mid-1963 in T-bills, the market, and strategies that trade on the quality signal, the value signal, and the joint quality and value signal. The top panel shows long/short strategies, which are levered each month to run at market volatility (i.e., an expected ex ante volatility of 16%, with leverage based on the observed volatility of the unlevered strategy over the preceding 60 months). By the end of 2011 a dollar invested in T-bills in 1963 would have grown to $12.31. A dollar invested in the market would have grown to $84.77. A dollar invested in the quality and value strategies would have grown to $94.04 and $35.12, respectively. A dollar invested in the strategy that traded on the joint quality and value signal would have grown to more than $2,131.

The bottom panel shows the performance of the long-only strategies. While a dollar invested in the market would have grown to more than $80, a dollar invested in profitable large cap stocks would have grown to $241, a dollar invested in cheap large cap stocks would have grown to $332, and a dollar invested in cheap, profitable large cap stocks would have grown to $572.

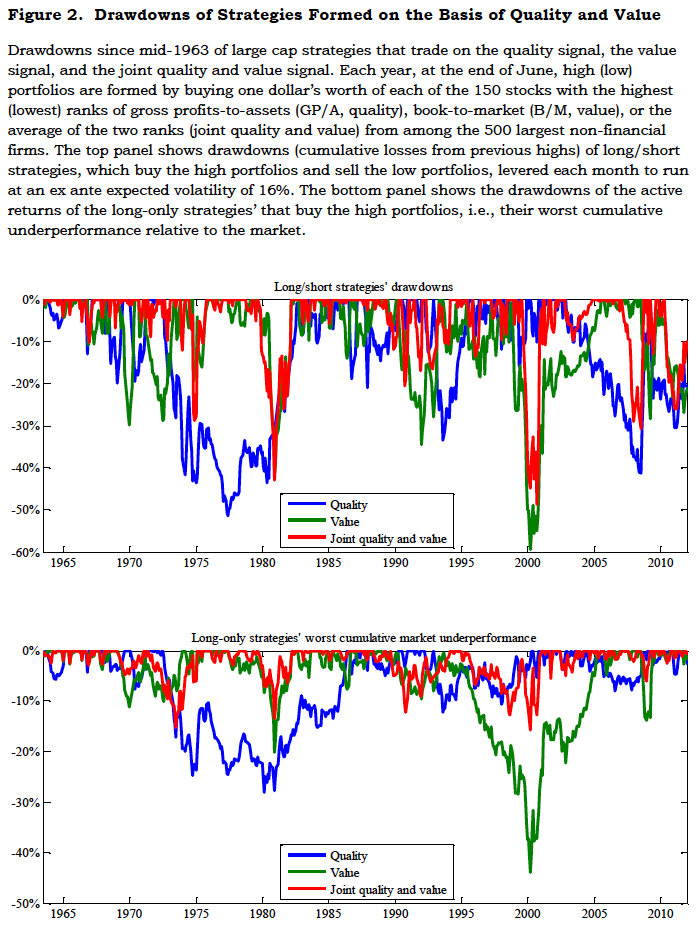

Drawdowns to Quality, Value, and Joint strategies

(Click to enlarge).

Figure 2 shows the drawdowns of the long/short strategies (top panel) and the worst cumulative under performance of the long-only strategies relative to the market, i.e., the drawdowns on the long-only strategies’ active returns (bottom panel). The top panel shows that the worst drawdowns experienced over the period by the long/short strategies run at market volatility were similar to market’s worst drawdown over the period. The joint quality and value strategy had, however, the smallest drawdowns of all the strategies considered. Its worst drawdown (48.7% in 2000) compares favorably to the worst drawdowns experienced by the market (51.6% in 2008-9, not shown), the traditional value strategy (down 59.5% by 2000), and the pure quality strategy (51.4% to 1977). Similar results hold for the worst five or ten drawdowns (average losses of 35.5% versus 41.1%, 38.9%, and 35.6% for the worst five drawdowns, and average losses of 25.8% versus 28.5%, 28.7%, and 26.5% for the worst ten drawdowns).

The bottom panel shows even more dramatic results for the long-only strategies active returns. Value stocks underperformed the market by 44% through the tech run-up over the second half of the ‘90s. Quality stocks lagged behind the market through much of the ‘70s, falling 28.1% behind by the end of the decade. Cheap, profitable stocks never lagged the market by more than 15.8%. Periods over which these stocks underperformed also tended to be followed quickly by periods of strong outperformance, yielding transient drawdowns that were sharply reversed.

Importantly, the signal in gross profitability is “extremely persistent,” and works well in the large cap universe.

Profitability strategies thus have low turnover, and can be implemented using liquid stocks with large capacities.

Novy-Marx’s basic message is that investors, in general but especially traditional value investors, leave money on the table when they ignore the quality dimension of value.

Read The Quality Dimension of Value Investing (.pdf).

Tomorrow, I show in an extract from Quantitative Value how we independently tested gross-profits-on-total-assets and found it to be highly predictive.

Read Full Post »