Capital management is a little understood, yet critical, issue for shareholder value creation. The research is clear: Investors should seek the rare companies with a manager like Henry Singleton–described by Warren Buffett as having “the best operating and capital deployment record in American business”–at the helm, who only buy back shares at trough valuations, are miserly with options, and only issue shares when the share price exceeds the stock’s intrinsic value. A manager who buys back stock at a peak valuation destroys value as surely as the manager who issues shares at a trough valuation.

It is a perplexing statistic, but, in aggregate, managers tend to buy back more stock at market peaks than at market troughs. It seems the average manager prefers to goose an already overvalued stock with a buyback at shareholder’s cost. In one of his recent commentaries, John Hussman noted that buybacks ebb and flow with the equity markets: when the markets are up, so are buybacks, and vice versa:

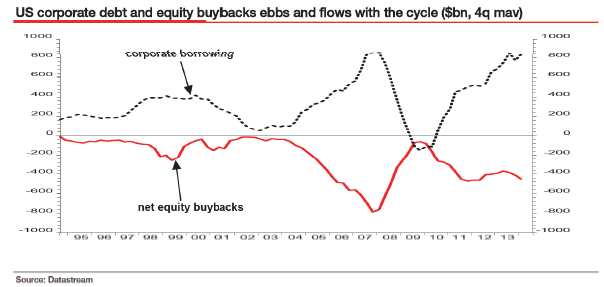

Notice that heavy equity buybacks (negative values on the red line below) are regularly financed by the issuance of corporate debt (a mirror image of positive values on the black line). Those debt-financed equity buybacks have been heaviest at market peaks like 1999-2000, 2007, and today. Put simply, the history of corporate stock buybacks is a chronicle of corporations buying stock with borrowed money at market tops, and retreating from buybacks at the very points that stocks are most reasonably valued.

He shares the following chart to illustrate his point:

Source: John Hussman, The Two Pillars of Full-Cycle Investing, September 8, 2014

This behavior turns the stomachs of value investors, but it’s par for the course for most managers. The Henry Singletons are few and far between. No manager focused on intrinsic value could behave this way.

These are sins of commission. Less visible, but equally impoverishing, are sins of omission: When undervalued, overcapitalized companies fail to grab a rare opportunity to buy back stock at a wide discount from intrinsic value. Where such unexploited opportunities exist, activists are incentivised to establish a position in the company and agitate to have management undertake a buyback. In Deep Value: Why Activist Investors and Other Contrarians Battle for Control of Losing Corporations (Wiley Finance, 2014), I examined one such example of an undervalued, overcapitalized company that failed to take its opportunity until two activists stepped up the pressure, and the outstanding returns that followed.

In early 2013 Carl Icahn began agitating to have Apple, Inc. use its enormous cash holding to buy back its very undervalued stock. Icahn would propose in an open letter to Tim Cook, Apple’s CEO, that Apple undertake a $150 billion buyback:

When we met, you agreed with us that the shares are undervalued. In our view, irrational undervaluation as dramatic as this is often a short-term anomaly. The timing for a larger buyback is still ripe, but the opportunity will not last forever. While the board’s actions to date ($60 billion share repurchase over three years) may seem like a large buyback, it is simply not large enough given that Apple currently holds $147 billion of cash on its balance sheet, and that it will generate $51 billion of EBIT next year (Wall Street consensus forecast).

…

With such an enormous valuation gap and such a massive amount of cash on the balance sheet, we find it difficult to imagine why the board would not move more aggressively to buy back stock by immediately announcing a $150 billion tender offer (financed with debt or a mix of debt and cash on the balance sheet).

Icahn believed that if Apple decided to borrow the full $150 billion at a 3 percent interest rate to undertake a tender at $525 per share, the result would be an immediate 33 percent boost to earnings per share and, assuming no multiple expansion, a commensurate 33 percent increase in the value of the shares. He saw the shares appreciating over the following three years from $525 to $1,250, assuming sustained 7.5 percent annual growth in Apple’s EBIT and an EBIT multiple of 11 from Apple’s 2013 EBIT multiple of 7. Icahn wasn’t the only activist to complain about Apple squandering an opportunity to buy back stock.

Around the same time Icahn sent his open letter to Cook, David Einhorn, speaking at the Ira W. Sohn Conference, also made an argument for Apple undertaking a buyback. Einhorn’s proposal was half the size of Icahn’s and didn’t require the company to take on debt. He noted that with close to $137 billion in cash on its balance sheet, Apple held more cash than “the market capitalization of all but 17 companies in the S&P 500,” the size of which “reveal[ed] a basic flaw in Apple’s capital allocation.” The problem with holding so much cash, according to Einhorn, was its opportunity cost. It earned only a small amount of interest, which meant a return below the rate of inflation. He likened it to “decaying inventory,” arguing that the real value of it declined a little bit every day:

Even worse, the return is far below the cost of capital. For companies with all-equity balance sheets, the cost of capital is particularly high, because expensive equity capital supports both the business and the foreign cash.

Finance theory suggests that an unlevered or net cash balance sheet should be rewarded with higher P/E multiples. In practice, the market assigns a discount for this level of overly conservative long-term capital management.

Not only does the cash earn a return below the cost of capital, it is evident that future profits will probably also be reinvested at a low return. As a result, the market not only discounts the cash sitting on the balance sheet, it also drives down the P/E multiple due to the anticipated suboptimal re-investment rate for future cash flows.

Einhorn argued that, at a 10 percent cost of capital, the cash represented an opportunity cost of close to $13.7 billion per year, or $14 in earnings per share.

Continue reading Buybacks: The Rationale and the Evidence article for the Manual of Ideas.

Buy Deep Value: Why Activist Investors and Other Contrarians Battle for Control of Losing Corporations (hardcover or Kindle, 240 pages, Wiley Finance) from Wiley Finance, Amazon, or Barnes and Noble.

Here’s your book for the fall if you’re on global Wall Street. Tobias Carlisle has hit a home run deep over left field. It’s an incredibly smart, dense, 213 pages on how to not lose money in the market. It’s your Autumn smart read. –Tom Keene, Bloomberg’s Editor-At-Large, Bloomberg Surveillance, September 9, 2014.

Click here if you’d like to read more on Deep Value, or connect with me on Twitter, LinkedIn or Facebook.

Your views that it’s best for companies to buy and sell their stock at lows and highs, respectively, are correct and backed up by empirical evidence. But I think you’re neglecting that one not-so-small reason that buys fail to happen at low prices is that the market lows typically occur during recessions and financial crises, which consequently dries up the possibility to borrow money. Since most companies do not have the huge cash pile that Apple had, and since profits and cash flows get beaten-down while borrowing becoming less available at such times, it could be practical impossibility rather than failure to understand value opportunity that at least partially drives the phenomenon.

LikeLike

Sure, but why then undertake buybacks at market peaks?

LikeLike

I agree; all evidence, including that which you refer to here, points to that companies’ boards and managers are as liable to buy and sell and the wrong time — let’s call it getting caught up in irrational exuberance — as anyone else (surprise, surprise!). My comment was not intended to refute that but rather serve as an additional explanation for the failure of buying at lows (admittedly it has less explanatory power for not selling at highs) which does not contradict yours. As so often in investing, there can be multiple factors with explanatory power. It is clear that boards and managers, being humans, make the same errors as most people do. But the few managers that can see through the manias and hysterias of the market and who understand that extreme overshoots both above and below for the economy are unlikely to remain forever, may in fact be restrained by lack of liquidity and borrowing availability if the market presents them with attractive buying opportunities.

LikeLike

Yes, I agree completely.

LikeLike

Hi Tobias,

I could agree more. Share buybacks speak volumes about the attitude and values of management. I’d add to your article that when a firm perceived to be in crisis buys back stock it sends a clear signal to investors that management is confident that the firm will move past its current problems.

http://www.oldschoolvalue.com/blog/investing-strategy/share-buybacks-outstanding-returns/

Those, along with insider buys during crisis, are great indicators.

PS. I look forward to picking up your book in the new year.

Evan

LikeLike

I suspect the majority of stock buy backs is simply to inflate the stock price so that management “stock” compensation is maximized. All disguised after all as shareholder value. The fact that stock buy backs fell off a cliff in 2008-2009 is rather telling since stocks as a whole then not get any cheaper than at that point in time. The other thing I find interesting is the lack of logical criteria’s to initiate the buy backs. I am not against the ideas as a whole but few seem to do it properly.

LikeLike

I agree.

LikeLike

[…] Activists can make money by agitating companies to buy back undervalued stock. (Greenbackd) […]

LikeLike