In 7-Footers In A Sea Of Pygmies: Why Concentrating On Just The Averages Obscures True Market Insights, Lonnie and Jacob from Farnam Street Investments have a great post on the current lack of dispersion in stock valuations. The corollary to last week’s post on the extremely tight distribution of P/E multiples for stocks in the S&P 500 (the tightest in 25 years) is that there are now fewer stocks with low P/Es than at any time in the last 25 years.

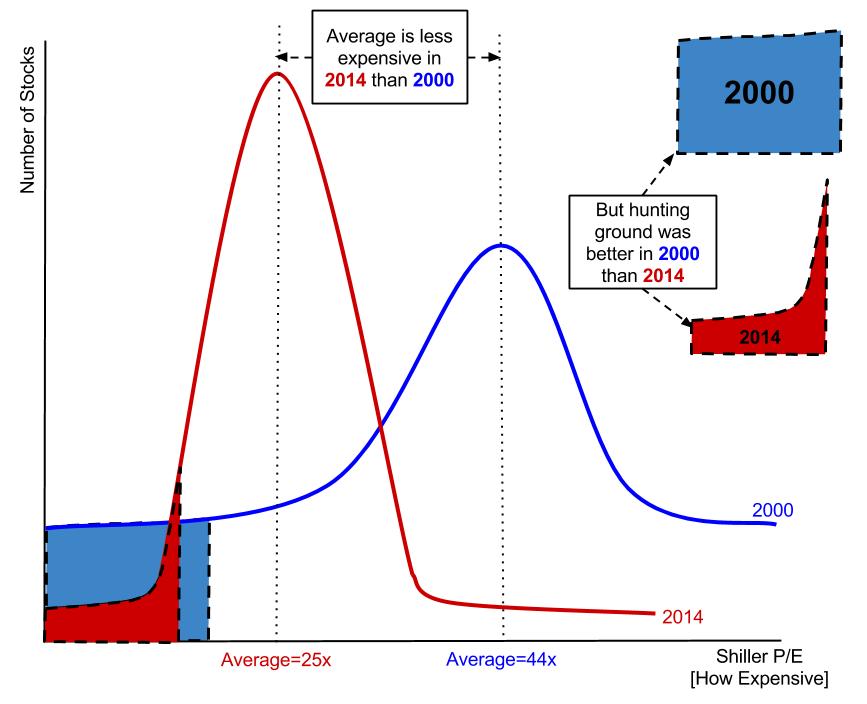

While the stock market peak in 2000 was higher than the current market (measured on the basis of the Shiller P/E ratio) the wider distribution of P/Es meant that there were many bargains available in 2000. Jacob and Lonnie write:

When there’s a wide range of cheap and expensive, the thoughtful investor can still find deals, even if the averages are generally high.

This is exactly what we saw in 2000 to 2001. Because of the disruptive arrival of the Internet, many stocks were priced to the moon, while some were being practically given away. The prevailing narrative was that new-economy internet stocks were the wave of the future and old-economy stocks were soon-to-be-extinct dinosaurs. This created a two-tiered market with a record high average price (the Shiller P/E was 44.2 in December 1999!), but a plethora of deals are available at the bottom. The chart below shows that time frame having a record high dispersion; it was a tribe with an incredibly wide range of heights to choose from.

What type of market do we find ourselves in today?

Looking back at our dispersion chart above, we’re currently at a 25-year low, meaning the cheapest 10% of the market looks an awful lot like the other 90%. And if you normalize earnings at all, the current P/E is extremely high with the Shiller CAPE at 25x. Prices are expensive and tightly packed around the average, meaning we shouldn’t expect very good returns from here. In fact by some statistical thresholds that we’ve already crossed, it’s one of the top five most dangerous markets of all time. It will be extremely difficult to be a stock picking hero in this environment. Even though the 2000 market average was higher than today, the 2000 time frame delivered a much better hunting ground.

Jacob and Lonnie conclude:

Value investors are known for ignoring “macro” developments and relying solely on their skills as bottom-up stock pickers. Their depth of research is usually unparalleled, but there’s a general hesitancy in considering broader market valuations in their analysis. We’re value investors through and through, but we think it’s a mistake not to pay attention to what the current investment opportunity set looks like compared to different points in history.

Read Farnam Street Investments’ 7-Footers In A Sea Of Pygmies: Why Concentrating On Just The Averages Obscures True Market Insights.

Order Quantitative Value from Wiley Finance, Amazon, or Barnes and Noble.

Click here if you’d like to read more on Quantitative Value, or connect with me on LinkedIn.

[…] low EBITDA yield, meaning it’s at an all-time high valuation. As we’ve seen previously (Worst value opportunity set in 25 years, and A Market of Stocks? Distribution of S&P 500 P/E Multiples Tightest In 25 Years), […]

LikeLike

[…] low EBITDA yield, meaning it’s at an all-time high valuation. As we’ve seen previously (Worst value opportunity set in 25 years, and A Market of Stocks? Distribution of S&P 500 P/E Multiples Tightest In 25 Years), […]

LikeLike

[…] February 20th, the blog Greenbackd highlighted research out of Farnam Street Investments which stated that, “there are now fewer […]

LikeLike

[…] https://greenbackd.com/2014/02/20/worst-value-opportunity-set-in-25-years/ […]

LikeLike

http://blog.alliancebernstein.com/index.php/2014/02/24/wallflower-value-stocks-are-ready-to-dance/

so there seem to be a difference in global stocks

LikeLike

[…] https://greenbackd.com/2014/02/20/worst-value-opportunity-set-in-25-years/ […]

LikeLike

[…] Art or science? Given that these are Shiller PE’s it should be remembered that the 2014 include the great 2007 profit slump https://greenbackd.com/2014/02/20/worst-value-opportunity-set-in-25-years/ […]

LikeLike

[…] Greenbackd (among others) notes that P/E dispersion is at the lowest level in 25 years. Readers should go to […]

LikeLike

[…] stock funds, pulling back on U.S. shares (WSJ) see also Worst Value Opportunity Set in 25 Years (Greenbackd) • Housing Weakness: Temporary or Enduring? (Calculated Risk) • The Perfectly Dangerous Thing […]

LikeLike

Where can one find this sort of P/E dispersion data? I’d like to monitor it in the future.

LikeLike

I have a feeling a lot of this lack of dispersion is due to people blindly buying indexes rather than active funds or individual companies. Great work, though!

LikeLike

A reasonable explanation, but more people are speculating in the market, indexes are not their favorite.

LikeLike

[…] Why the dispersion of valuation matters more than average. (Greenbackd) […]

LikeLike

Absolutely best article I have seen this year.

LikeLike